Imagine some years ago you changed jobs and left in your previous employer’s pension scheme a defined benefit (sometimes called a final salary) pension.

You have recently received a statement from the scheme telling you the current value of your annual pension payable at retirement.

The administrators have also told you the current capital value of that pension benefit.

It’s called a cash equivalent transfer value (CETV) and you were astonished by just how much it was, almost as much as a small lottery win!

Your instinct is to have that cash equivalent transfer value moved into your personal pension plan. But is that the right thing to do?

Before you transfer there are some important questions to ask yourself. Most importantly should you be giving up a guaranteed income for life when you reach retirement in return for a less defined retirement income?

Equally as important might be the question should you be giving up a guaranteed income for your spouse if I were to die?

The answer is, it depends.

What you need to work out is if the deferred final salary pension is worth more to you and your family than the transfer value into a personal pension plan.

The way to answer these important questions is through a process. That process is known as financial planning.

An important part of that process is called lifetime cash flow forecasting.

Lifetime cash flow forecasting is an essential part of defined benefit transfer advice. Share on XWhat this does is to look at your income and expenditure now and into the future. It looks at your assets and liabilities as well.

It calculates the answer to the question, “Will I ever run out of money?”

You may have other needs and wants for example a lump sum to pay off the outstanding mortgage or perhaps help the kids onto the property ladder. You may even want to retire much earlier than the scheme retirement age.

Sometimes the right answer is to keep the deferred pension in the scheme and then take that income (or tax free cash lump sum and reduced income) when you retire. Sometimes the answer is to transfer to a personal pension plan and flexibly access those benefits.

Without carrying out the lifetime cash flow forecast it is often difficult to know what to do.

Transferring out of a defined benefits scheme does involve investment risk (you take on that risk rather than your previous employer) and you do need to be aware of the degree of risk involved before you transfer.

But financial planning and the life time cash flow forecast will help to establish if a transfer is suitable for you.

There are a lot of numbers to be crunched but to help you understand what is right for you we can convert those numbers into a chart to show you visually what they mean. Here’s an example.

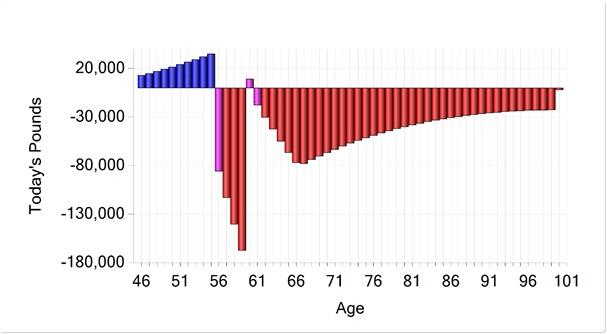

Scenario One – You retain your DB benefits and retire at age 56.

Value of Liquid Assets:

The red lines in the bar chart demonstrate that remaining in the scheme and taking the benefits from that scheme will not allow you to retire early and enjoy the lifestyle that you require.

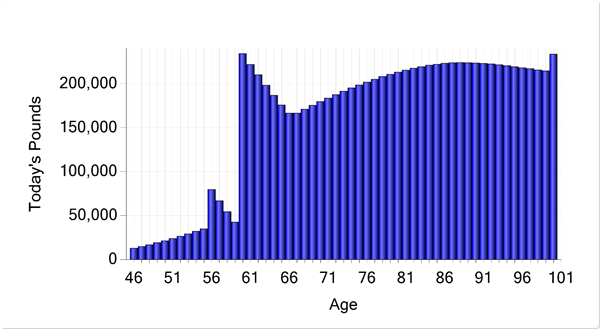

Scenario Two – You transfer your DB value to a money purchase arrangement and retire at age 56.

Value of Liquid Assets:

This chart demonstrate that to achieve your financial goals and objectives there is a significantly greater chance of success by giving up the guaranteed deferred pension benefits and the lower available tax free cash lump sum and transferring now to a personal pension plan.

What is important is suitability and that is different for each person. Financial Planning results in a bespoke outcome for you.